Family Foundations - Overview Structure and Tax Treatment

Understanding family foundations structure and tax treatment

CORPORATE TAX (CT)

What is a Family Foundation?

A Family Foundation is not a specific legal entity type in the UAE but a concept for Corporate Tax purposes. It is defined as a foundation, trust, or similar entity that meets specific conditions in the Corporate Tax Law (Article 17(1)).

Its primary purpose is for families to manage and preserve wealth across generations (e.g. holds share investments or holds real estate investments).

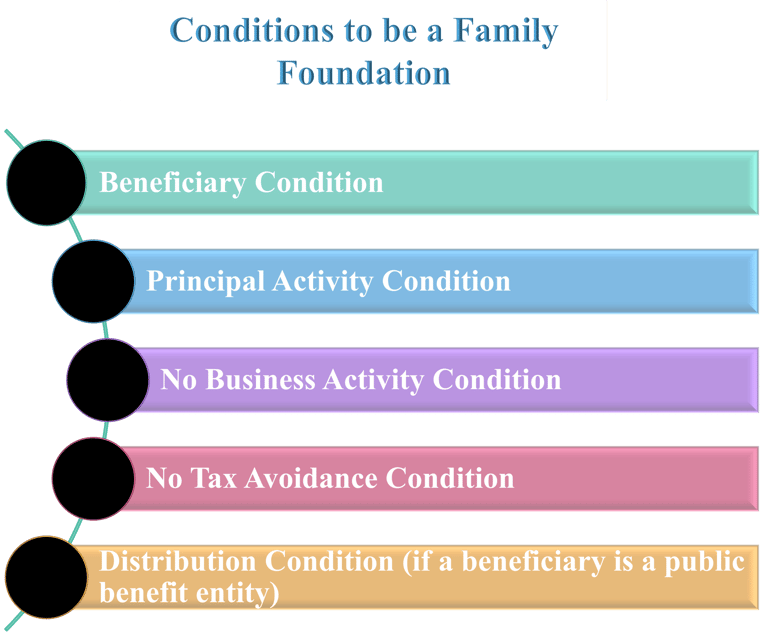

Conditions to be a Family Foundation (Article 17(1) of CT Law)

To qualify as a Family Foundation and be eligible to apply for fiscally transparent status, an entity must meet all of the following five conditions:

1. Beneficiary Condition

The entity must be established for the benefit of:

Identified / Identifiable natural persons (named individuals, or a class like "all future grandchildren"), or

A public benefit entity (e.g., a charitable organization), or

A combination of the above.

2. Principal Activity Condition

The entity's main activity must be to receive, hold, invest, disburse, or otherwise manage assets or funds associated with savings or investments.

3. No Business Activity Condition

The entity must not conduct any activity that would be considered a "Business or Business Activity" if it were carried out directly by its founder, settlor, or any of its natural person beneficiaries.

It can undertake activities that qualify as Personal Investment or Real Estate Investment for a natural person (which are outside the scope of Corporate Tax), such as renting out real estate without needing a commercial license.

4. No Tax Avoidance Condition

The main purpose of the entity must not be the avoidance of Corporate Tax.

5. Distribution Condition (if a beneficiary is a public benefit entity)

This condition only applies if one or more beneficiaries is a public benefit entity.

In such a case, the entity must meet one of the following:

a) The public benefit entity does not derive any Taxable Income through the Family Foundation (e.g., all its income is Exempt Income, or it is a Qualifying Public Benefit Entity).

b) Any Taxable Income attributable to the public benefit entity is distributed to it within 6 months from the end of the Tax Period.

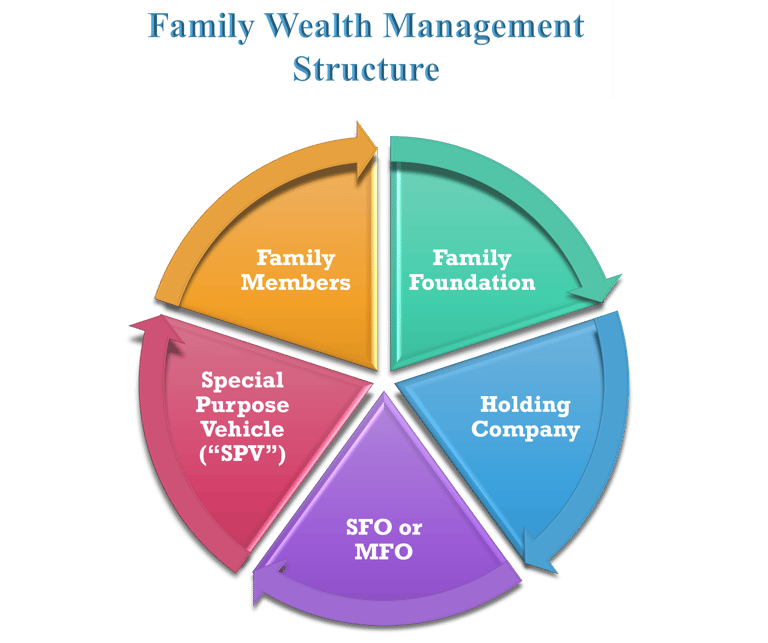

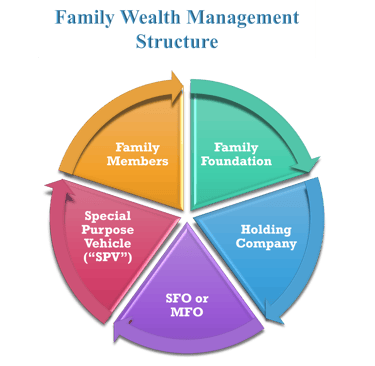

Family Wealth Management Structure:

Typically includes the following entities:

1. a Family Foundation.

2. a holding company: wholly owned and controlled directly or indirectly by a Family Foundation whose primary purpose is to own and hold investments. It typically sits within a family wealth structure to own other entities, such as Special Purpose Vehicles (SPVs).

3. a Special Purpose Vehicle (“SPV”): wholly owned and controlled directly or indirectly by a Family Foundation are used to segregate different types of investments, such as one SPV holding only share investments and another holding only real estate investments.

4. a SFO or MFO:

SFO (Single Family Office): An entity, typically a juridical person, established to provide wealth and investment management services exclusively for a single family and its related foundation and entities.

MFO (Multi Family Office): An entity, typically a juridical person, that was set up to service more than one family.

Both SFOs and MFOs provide services such as "family office services", "wealth and investment management services," and "fund management services." They are usually remunerated via management fees for the services provided.

5. Family Members: are the natural persons (individuals) who are the ultimate beneficiaries of the Family Foundation and the entire wealth management structure.

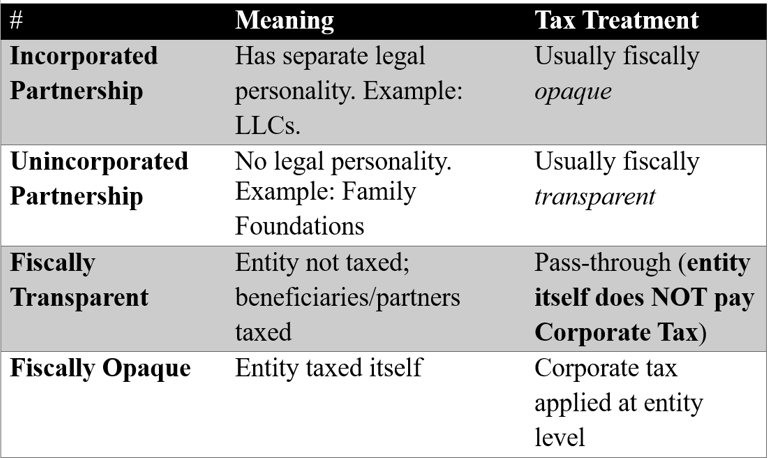

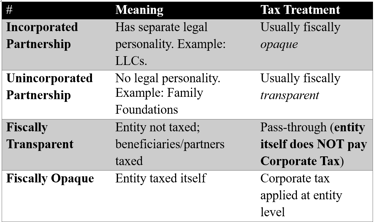

Quick Comparison of Incorporated and Unincorporated partnerships, Fiscally transparent and Fiscally Opaque:

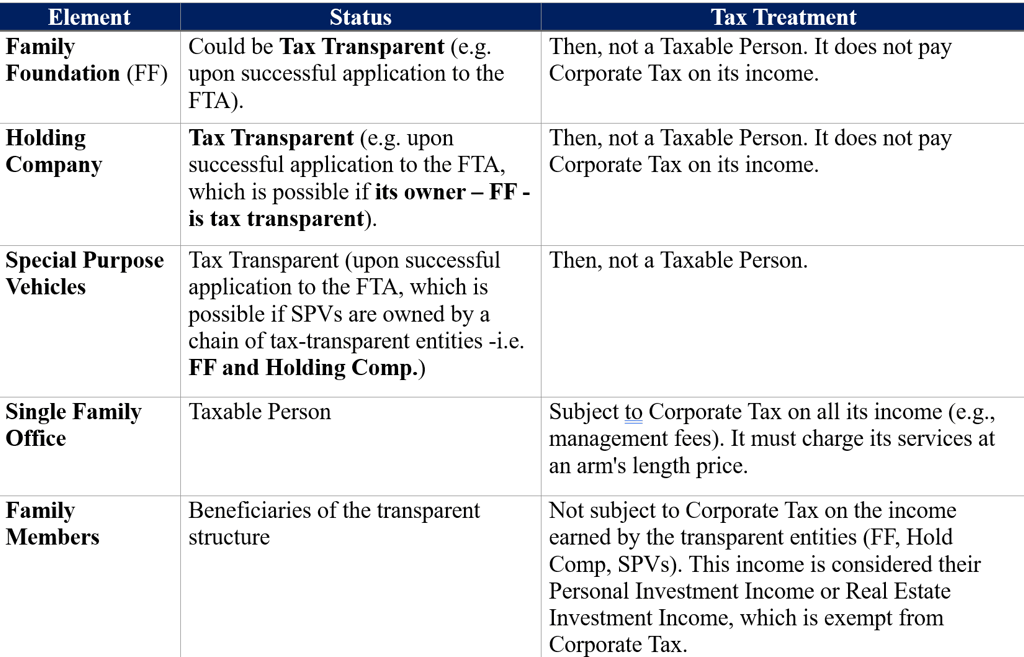

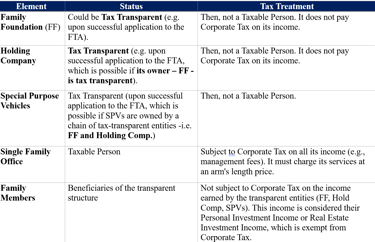

Best Case Scenario of Tax Treatment of Each Element of The Family Wealth Management Structure:

Key Takeaways:

The UAE Federal Tax Authority's (FTA) recent public clarification provides critical guidance for families managing their wealth which requires detailed analysis on a case by case basis.

Need help understanding your UAE CT obligations? Contact Assure Gate Tax & Accounts for expert guidance tailored to your business.